Table of contents

Forecasting of sales by the Prophet

The aim was to create a model prediction of the sales for the next three weeks. Currently, the sales forecast is set 3 weeks ahead based on last week’s sales. The Weighted Absolute Percent Error (WAPE) is used for comparison purposes.

The whole dataset contains 3 CSV files.

The first is sales.csv: Data on product-level weekly sales.

- week_starting_date - the first day of the week date in format YYYYMMDD

- product_id - unique id for the product

- sales - weekly sales in pieces

The second is categories.csv: Data on which categories products are assigned to.

- product_id - unique id for the product

- category_id - unique id for category

The third is traffic.csv

- week_starting_date - the first day of the week date in format YYYYMMDD

- product_id - unique id for the product

- traffic - weekly product displays on the website

from google.colab import drive

drive.mount('/content/gdrive')

Mounted at /content/gdrive

sales.csv

import datetime

import pandas as pd

import numpy as np

sales = pd.read_csv('gdrive/My Drive/Prediction_task/sales.csv', sep=';')

sales.head()

| week_starting_date | product_id | sales | |

|---|---|---|---|

| 0 | 20191209 | 1990 | 1 |

| 1 | 20201123 | 1990 | 1 |

| 2 | 20201207 | 1990 | 1 |

| 3 | 20191202 | 1990 | 1 |

| 4 | 20201109 | 1990 | 2 |

Data cleaning

# Change week_starting_date to YYYY-DD-MM format

sales['week_starting_date'] = (sales['week_starting_date']

.apply(lambda x: pd.to_datetime(str(x), format='%Y%m%d')))

print(sales)

week_starting_date product_id sales

0 2019-12-09 1990 1

1 2020-11-23 1990 1

2 2020-12-07 1990 1

3 2019-12-02 1990 1

4 2020-11-09 1990 2

... ... ... ...

105776 2020-10-05 567 9

105777 2020-09-28 567 16

105778 2020-12-07 2643 6

105779 2020-12-14 2643 5

105780 2020-11-30 2643 19

[105781 rows x 3 columns]

def fill_missing_data(df: pd.DataFrame, column: str) -> pd.DataFrame:

"""

Fill in missing values. When there are missing sales for some date,

the assumption is that there was no sale of the product.

Input:

df: pd.DataFrame,

column: str

Output:

filled_missing_sales: pd.DataFrame

"""

filled_missing_sales = df.set_index(

['week_starting_date', column]

).unstack(

fill_value=0

).asfreq(

'W-MON', fill_value=0

).stack().reset_index()

return filled_missing_sales

filled_missing_sales = fill_missing_data(sales, 'product_id')

# Checking one of the product sales

new_df = filled_missing_sales.loc[filled_missing_sales['product_id'] == 48]

new_df = new_df[['week_starting_date', 'sales']]

print(new_df)

week_starting_date sales

43 2019-01-07 4

2969 2019-01-14 0

5895 2019-01-21 27

8821 2019-01-28 32

11747 2019-02-04 3

... ... ...

289717 2020-11-30 30

292643 2020-12-07 25

295569 2020-12-14 50

298495 2020-12-21 32

301421 2020-12-28 28

[104 rows x 2 columns]

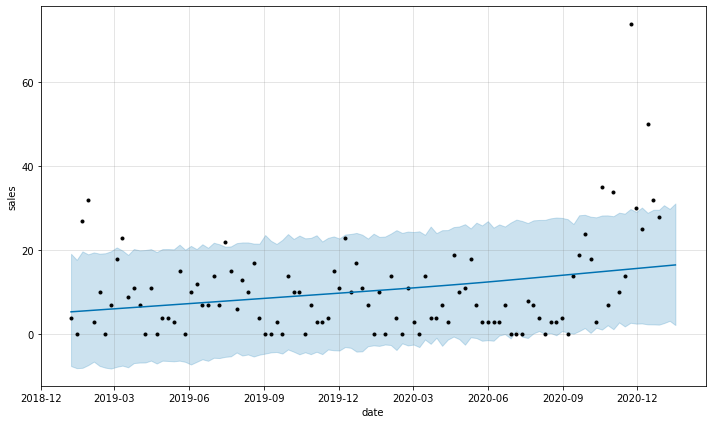

Create first prophet model for chosen product

# Import prophet to create model using this library

import fbprophet

# Sample model for chosen product_id. By default prophet use linear model

m = fbprophet.Prophet()

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'sales': 'y'})

m.fit(new_df)

# Forecast for following 3 weeks

future = m.make_future_dataframe(3, freq='W')

forecast = m.predict(future)

fig = m.plot(forecast, ylabel='sales', xlabel='date')

INFO:fbprophet:Disabling yearly seasonality. Run prophet with yearly_seasonality=True to override this.

INFO:fbprophet:Disabling weekly seasonality. Run prophet with weekly_seasonality=True to override this.

INFO:fbprophet:Disabling daily seasonality. Run prophet with daily_seasonality=True to override this.

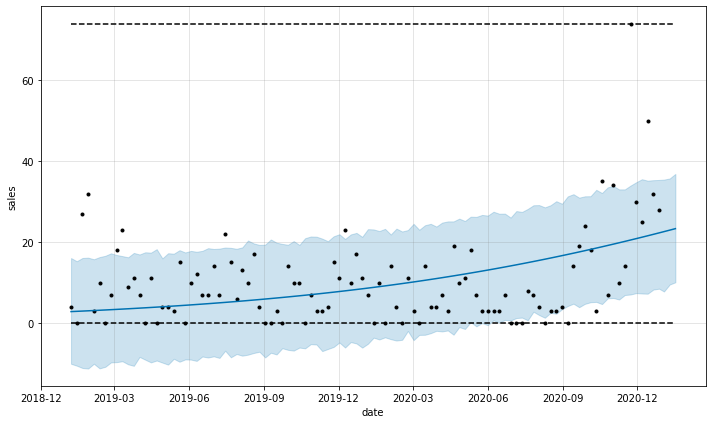

# Create model with logistic regression

m = fbprophet.Prophet(growth = 'logistic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'sales': 'y'})

# Set floor and cap for the dataset and forecast in order to use logistic model

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

forecast = m.predict(future)

fig = m.plot(forecast, ylabel='sales', xlabel='date')

INFO:fbprophet:Disabling yearly seasonality. Run prophet with yearly_seasonality=True to override this.

INFO:fbprophet:Disabling weekly seasonality. Run prophet with weekly_seasonality=True to override this.

INFO:fbprophet:Disabling daily seasonality. Run prophet with daily_seasonality=True to override this.

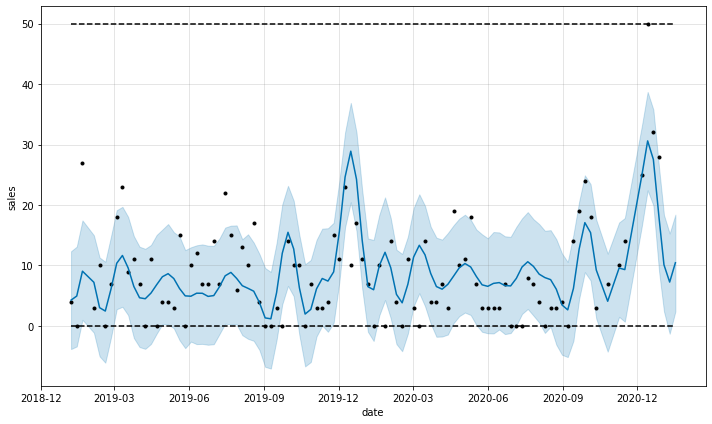

Further data cleaning

from datetime import datetime as dt

from datetime import timedelta as td

def remove_outliers(df: pd.DataFrame, item: str) -> pd.DataFrame:

"""

Removing outliers by calculating 0.95 quantile per product

Input: df: pd.DataFrame

item: str

Output: pd.DataFrame

"""

today = filled_missing_sales.week_starting_date.max()

delta = td(weeks=2)

date_cutoff = today - delta

date_cutoff = date_cutoff.strftime('%Y-%m-%d')

# Get data from the beginning to the three weeks before the max of available date

mask = (df['week_starting_date'] <date_cutoff)

df_without_december = df.loc[mask]

# Get data from last 3 weeks

mask2 = (df['week_starting_date'] >= date_cutoff)

df_with_december = df.loc[mask2]

# Remove outliers from the "training" dataset

q = (df_without_december.groupby('product_id')[item]

.transform(lambda x: x.quantile(.95)))

df_without_december = (

df_without_december[df_without_december.sales <= q])

# Concat cleaned training and test dataset

frames = [df_without_december, df_with_december]

result = pd.concat(frames)

return result

filled_missing_sales = remove_outliers(filled_missing_sales, 'sales')

# Plot of the dataset with removed outliers for chosen product_id

# and set yearly_seasonality=True

new_df = filled_missing_sales.loc[filled_missing_sales['product_id'] == 48]

new_df = new_df[['week_starting_date', 'sales']]

m = fbprophet.Prophet(yearly_seasonality=True, growth = 'logistic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'sales': 'y'})

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

forecast = m.predict(future)

fig = m.plot(forecast, ylabel='sales', xlabel='date')

INFO:fbprophet:Disabling weekly seasonality. Run prophet with weekly_seasonality=True to override this.

INFO:fbprophet:Disabling daily seasonality. Run prophet with daily_seasonality=True to override this.

Create models for all products

from fbprophet.diagnostics import performance_metrics, cross_validation

import random

import logging

logging.getLogger('fbprophet').setLevel(logging.WARNING)

def get_date_as_str(df: pd.DataFrame, week: int, type_return: str) -> str:

"""

Get date based on ds column from the dataframe for chosen delta week

Input:

df: pd.DataFrame

week: int

Output:

date_cutoff: str

"""

date = df.ds.max()

delta = td(weeks=week)

date_cutoff = date - delta

date_cutoff = date_cutoff.strftime('%Y-%m-%d')

if type_return == 'type_datetime':

date_cutoff = pd.to_datetime([str(date_cutoff)])

return date_cutoff

def get_prediction(df: pd.DataFrame, seasonality_prior: int, cap_multiplier: int, changepoint_prior: int) -> dict:

"""

Create prediction for products sales.

In this model has been chosen short-term analysis of the data

(16 weeks before the last available date).

Input:

df: pd.DataFrame

seasonality_prior: int (multiplier of max cap)

cap_multiplier: int (seasonality_prior_scale)

changepoint_prior: int

Output:

prediction: dict

"""

prediction = {}

df = df.rename(columns={'week_starting_date': 'ds','sales': 'y', 'product_id': 'article'})

list_articles = df.article.unique()

random.seed(100)

list_articles = random.sample(list(list_articles), 100)

for article in list_articles:

# To check model performance for first product_id, the break func

# has been used

#if article >= 200:

# break

article_df = df.loc[df['article'] == article].copy()

article_df['cap'] = cap_multiplier * max(article_df.y)

article_df['floor'] = 0

# Check if the cap is equal the floor

if max(article_df.y) != 0:

my_model = fbprophet.Prophet(weekly_seasonality=True,

seasonality_prior_scale=seasonality_prior,

changepoint_prior_scale=changepoint_prior,

growth = 'logistic')

# Filter date from 16 weeks of the last record to last record

cutoffs = get_date_as_str(df = article_df,

week = 16,

type_return = "type_str")

mask = (article_df['ds'] >=cutoffs)

article_df = article_df.loc[mask]

my_model.fit(article_df)

#df_cv = cross_validation(my_model, initial='548 days', period='180 days', horizon = '21 days')

#df_cv = cross_validation(my_model, initial='695 days', period='7 days', horizon = '21 days')

# Set cutoff date 3 weeks of the last record

cutoffs = get_date_as_str(df = article_df,

week = 3,

type_return = "type_datetime")

df_cv = cross_validation(my_model,

cutoffs=cutoffs,

horizon='21 days',

parallel="threads")

# Round predicted values and replace if is negative

df_cv.yhat = df_cv.yhat.round()

df_cv.yhat = df_cv.yhat.mask(df_cv.yhat.lt(0),0)

del my_model

else:

data = ([['2020-12-14', 0, 0],

['2020-12-21', 0, 0],

['2020-12-28', 0, 0]])

df_cv = pd.DataFrame(data, columns = ['ds', 'y', 'yhat'])

#future_dates = my_model.make_future_dataframe(periods=3, freq='W')

#forecast = my_model.predict(future_dates)

prediction[article] = df_cv

return prediction

def calc_diffrenece_wape(df: dict, filled_missing_sales: pd.DataFrame):

"""

Calculate the WAPE. For the prophet forecast, it is one subfunction, and the

basic forecast is another subfunction. Basic forecast estimates the sales in

next following three weeks will be on the same level as in the last week.

There was also made one modification, that to the nominator and denominator

have been added one, to avoid dividing by zero, so the WAPE values resulted

from these functions will be different than in the original WAPE indicator.

Input: df: dict

filled_missing_sales: pd.DataFrame

Output:

len(predicted.keys()): int

prophet_better: int

"""

prophet_better = 0

basic_better = 0

same_results = 0

def calc(df):

table_wape = {}

result_nom = 1

result_denom = 1

for i in range(0, len(df)):

result_nom = result_nom + abs(df['yhat'][i]-df['y'][i])

result_denom = result_denom + abs(df['y'][i])

return result_nom/result_denom

def calc_original_df(df, j):

df = (df.loc[(df.product_id == j) &

(df.week_starting_date>='2020-12-07'),

['sales', 'week_starting_date']])

table_wape = {}

result_nom = 1

result_denom = 1

df = df.reset_index()

for i in range(0, len(df)-1):

result_nom = result_nom + abs(df['sales'][i+1]-df['sales'][i])

result_denom = result_denom + abs(df['sales'][i+1])

return result_nom/result_denom

for j in predicted.keys():

wape_prophet = calc(df[j])

wape_original = calc_original_df(filled_missing_sales, j)

#print(wape_prophet, wape_original)

# Compare if the prophet wape ratio is not worse than for basic model

if wape_prophet < wape_original:

prophet_better+=1

elif wape_prophet == wape_original:

same_results+=1

elif wape_prophet > wape_original:

basic_better+=1

return len(predicted.keys()), prophet_better, same_results, basic_better

Tuning hyperparameters

Parameters that can be tuned are available on the prophet website https://facebook.github.io/prophet/docs/diagnostics.html#hyperparameter-tuning

seasonality_prior=[0.01, 0.1, 1, 10]

cap_multiplier=[0.25, 0.5, 1]

changepoint_prior=[0.001, 0.01, 0.1, 0.5]

for selected_seasonality_prior in seasonality_prior:

for selected_cap_multiplier in cap_multiplier:

for selected_changepoint_prior in changepoint_prior:

predicted = get_prediction(filled_missing_sales,

selected_seasonality_prior,

selected_cap_multiplier,

selected_changepoint_prior)

products, prophet_better, same_results, basic_better = calc_diffrenece_wape(predicted, filled_missing_sales)

print("Prophet achieved better result for " +

str(round(prophet_better/products*100)) + "% of cases (WAPE performance metric)")

print("Prophet achieved the same result for " +

str(round(same_results/products*100)) + "% of cases (WAPE performance metric)")

print("Prophet achieved worse result for " +

str(round(basic_better/products*100)) + "% of cases (WAPE performance metric)")

Prophet achieved better result for 45% of cases (WAPE performance metric)

Prophet achieved the same result for 26% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 30% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 42% of cases (WAPE performance metric)

Prophet achieved the same result for 22% of cases (WAPE performance metric)

Prophet achieved worse result for 36% of cases (WAPE performance metric)

Prophet achieved better result for 38% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 38% of cases (WAPE performance metric)

Prophet achieved better result for 37% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 39% of cases (WAPE performance metric)

Prophet achieved better result for 36% of cases (WAPE performance metric)

Prophet achieved the same result for 25% of cases (WAPE performance metric)

Prophet achieved worse result for 39% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 30% of cases (WAPE performance metric)

Prophet achieved better result for 45% of cases (WAPE performance metric)

Prophet achieved the same result for 27% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 48% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 30% of cases (WAPE performance metric)

Prophet achieved better result for 44% of cases (WAPE performance metric)

Prophet achieved the same result for 28% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 44% of cases (WAPE performance metric)

Prophet achieved the same result for 28% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 44% of cases (WAPE performance metric)

Prophet achieved the same result for 29% of cases (WAPE performance metric)

Prophet achieved worse result for 27% of cases (WAPE performance metric)

Prophet achieved better result for 39% of cases (WAPE performance metric)

Prophet achieved the same result for 25% of cases (WAPE performance metric)

Prophet achieved worse result for 36% of cases (WAPE performance metric)

Prophet achieved better result for 38% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 38% of cases (WAPE performance metric)

Prophet achieved better result for 36% of cases (WAPE performance metric)

Prophet achieved the same result for 25% of cases (WAPE performance metric)

Prophet achieved worse result for 39% of cases (WAPE performance metric)

Prophet achieved better result for 36% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 40% of cases (WAPE performance metric)

Prophet achieved better result for 47% of cases (WAPE performance metric)

Prophet achieved the same result for 22% of cases (WAPE performance metric)

Prophet achieved worse result for 31% of cases (WAPE performance metric)

Prophet achieved better result for 45% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 32% of cases (WAPE performance metric)

Prophet achieved better result for 45% of cases (WAPE performance metric)

Prophet achieved the same result for 26% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 46% of cases (WAPE performance metric)

Prophet achieved the same result for 26% of cases (WAPE performance metric)

Prophet achieved worse result for 28% of cases (WAPE performance metric)

Prophet achieved better result for 44% of cases (WAPE performance metric)

Prophet achieved the same result for 27% of cases (WAPE performance metric)

Prophet achieved worse result for 29% of cases (WAPE performance metric)

Prophet achieved better result for 41% of cases (WAPE performance metric)

Prophet achieved the same result for 27% of cases (WAPE performance metric)

Prophet achieved worse result for 32% of cases (WAPE performance metric)

Prophet achieved better result for 41% of cases (WAPE performance metric)

Prophet achieved the same result for 27% of cases (WAPE performance metric)

Prophet achieved worse result for 32% of cases (WAPE performance metric)

Prophet achieved better result for 41% of cases (WAPE performance metric)

Prophet achieved the same result for 28% of cases (WAPE performance metric)

Prophet achieved worse result for 31% of cases (WAPE performance metric)

Prophet achieved better result for 39% of cases (WAPE performance metric)

Prophet achieved the same result for 26% of cases (WAPE performance metric)

Prophet achieved worse result for 35% of cases (WAPE performance metric)

Prophet achieved better result for 38% of cases (WAPE performance metric)

Prophet achieved the same result for 24% of cases (WAPE performance metric)

Prophet achieved worse result for 38% of cases (WAPE performance metric)

Prophet achieved better result for 38% of cases (WAPE performance metric)

Prophet achieved the same result for 25% of cases (WAPE performance metric)

Prophet achieved worse result for 37% of cases (WAPE performance metric)

Prophet achieved better result for 38% of cases (WAPE performance metric)

Prophet achieved the same result for 26% of cases (WAPE performance metric)

Prophet achieved worse result for 36% of cases (WAPE performance metric)

Prophet achieved better result for 46% of cases (WAPE performance metric)

Prophet achieved the same result for 23% of cases (WAPE performance metric)

Prophet achieved worse result for 31% of cases (WAPE performance metric)

Reducing the upper limit by using a scaling parameter smaller than one, improved the WAPE index.

# Display some metrics generated by the cross_validation function

# eg. product_id=5

df_p = performance_metrics(predicted[5])

df_p

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

<ipython-input-2-cad13214df58> in <module>()

3 # Display some metrics generated by the cross_validation function

4 # eg. product_id=5

----> 5 df_p = performance_metrics(predicted[5])

6 df_p

NameError: name 'predicted' is not defined

Unfortunately due to a killed session in colab after several hours of model validation, the individual parameters cannot be displayed from the ready-made performance_metrics function

If some product has insufficient sales data (for example it is some kind of new product in the store), take the period of sales per the category.

categories.csv

categories = pd.read_csv('gdrive/My Drive/Prediction_task/categories.csv', sep=';')

categories.head()

| product_id | category_id | |

|---|---|---|

| 0 | 1990 | 0 |

| 1 | 2361 | 1 |

| 2 | 1085 | 2 |

| 3 | 3091 | 3 |

| 4 | 955 | 4 |

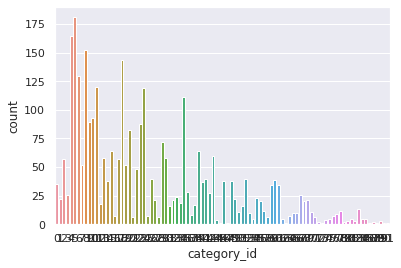

Investigation of the categories dataset

categories_agg = (categories[['product_id', 'category_id']]

.groupby(['category_id'])

.agg(['count']))

categories_agg

| product_id | |

|---|---|

| count | |

| category_id | |

| 0 | 35 |

| 1 | 22 |

| 2 | 57 |

| 3 | 26 |

| 4 | 165 |

| ... | ... |

| 87 | 2 |

| 88 | 1 |

| 89 | 3 |

| 90 | 1 |

| 91 | 1 |

92 rows × 1 columns

import seaborn as sns

sns.set_theme(style="darkgrid")

ax = sns.countplot(x="category_id", data=categories)

joined_df = filled_missing_sales.merge(categories)

joined_df.head()

| week_starting_date | product_id | sales | category_id | |

|---|---|---|---|---|

| 0 | 2019-01-07 | 1 | 0 | 10 |

| 1 | 2019-01-14 | 1 | 0 | 10 |

| 2 | 2019-01-21 | 1 | 0 | 10 |

| 3 | 2019-01-28 | 1 | 0 | 10 |

| 4 | 2019-02-04 | 1 | 0 | 10 |

grouped_joined_df = (joined_df

.groupby(['week_starting_date','category_id'])

['sales'].sum().reset_index())

grouped_joined_df

| week_starting_date | category_id | sales | |

|---|---|---|---|

| 0 | 2019-01-07 | 0 | 38 |

| 1 | 2019-01-07 | 1 | 44 |

| 2 | 2019-01-07 | 2 | 68 |

| 3 | 2019-01-07 | 3 | 47 |

| 4 | 2019-01-07 | 4 | 237 |

| ... | ... | ... | ... |

| 9522 | 2020-12-28 | 87 | 0 |

| 9523 | 2020-12-28 | 88 | 0 |

| 9524 | 2020-12-28 | 89 | 0 |

| 9525 | 2020-12-28 | 90 | 0 |

| 9526 | 2020-12-28 | 91 | 0 |

9527 rows × 3 columns

def get_prediction_category(df: pd.DataFrame) -> dict:

"""

Create prediction for category sales

Input:

df: pd.DataFrame

Output:

prediction: dict

"""

prediction = {}

df = df.rename(columns={'week_starting_date': 'ds',

'sales': 'y',

'category_id': 'category'})

list_categories = df.category.unique()

for category in list_categories:

category_df = df.loc[df['category'] == category].copy()

category_df['cap'] = 0.5 * max(category_df.y)

category_df['floor'] = 0

if max(category_df.y)!=0:

my_model = fbprophet.Prophet(yearly_seasonality=True,

seasonality_prior_scale=1.0,

growth = 'logistic')

my_model.fit(category_df)

#df_cv = cross_validation(my_model, initial='548 days', period='180 days', horizon = '21 days')

#df_cv = cross_validation(my_model, initial='695 days', period='7 days', horizon = '21 days')

# Set cutoff date 3 weeks of the last record

cutoffs = get_date_as_str(df = category_df,

week = 3,

type_return = "type_datetime")

df_cv = cross_validation(my_model, cutoffs=cutoffs, horizon='21 days')

# replace less than 0 values and round it

df_cv.yhat = df_cv.yhat.round()

df_cv.yhat = df_cv.yhat.mask(df_cv.yhat.lt(0),0)

#future_dates = my_model.make_future_dataframe(periods=3, freq='W')

#forecast = my_model.predict(future_dates)

prediction[category] = df_cv

del my_model

else:

data = ([['2020-12-14', 0, 0],

['2020-12-21', 0, 0],

['2020-12-28', 0, 0]])

df_cv = pd.DataFrame(data, columns = ['ds', 'y', 'yhat'])

return prediction

predicted_joined = get_prediction_category(grouped_joined_df)

traffic.csv

traffic = pd.read_csv('gdrive/My Drive/Prediction_task/traffic.csv', sep=';')

traffic['week_starting_date'] = (traffic['week_starting_date']

.apply(lambda x: pd.to_datetime(str(x), format='%Y%m%d')))

traffic.head()

| week_starting_date | product_id | traffic | |

|---|---|---|---|

| 0 | 2019-01-07 | 1990 | 1 |

| 1 | 2019-01-07 | 2361 | 7 |

| 2 | 2019-01-07 | 1085 | 1 |

| 3 | 2019-01-07 | 3091 | 4 |

| 4 | 2019-01-07 | 955 | 12 |

sales_filled = fill_missing_data(sales, 'product_id')

new_df_merged = pd.merge(sales_filled,

traffic,

how='outer',

left_on=['week_starting_date','product_id'],

right_on = ['week_starting_date','product_id'])

new_df_merged

| week_starting_date | product_id | sales | traffic | |

|---|---|---|---|---|

| 0 | 2019-01-07 | 1 | 0.0 | NaN |

| 1 | 2019-01-07 | 2 | 0.0 | NaN |

| 2 | 2019-01-07 | 3 | 0.0 | NaN |

| 3 | 2019-01-07 | 4 | 0.0 | NaN |

| 4 | 2019-01-07 | 5 | 0.0 | NaN |

| ... | ... | ... | ... | ... |

| 304388 | 2020-12-14 | 1105 | NaN | 1.0 |

| 304389 | 2020-12-21 | 831 | NaN | 1.0 |

| 304390 | 2020-12-21 | 1203 | NaN | 1.0 |

| 304391 | 2020-12-21 | 2540 | NaN | 1.0 |

| 304392 | 2020-12-28 | 831 | NaN | 1.0 |

304393 rows × 4 columns

Data cleaning

new_df_merged['traffic'] = new_df_merged['traffic'].fillna(0).astype(int)

new_df_merged['sales'] = new_df_merged['sales'].fillna(0).astype(int)

new_df_merged

| week_starting_date | product_id | sales | traffic | |

|---|---|---|---|---|

| 0 | 2019-01-07 | 1 | 0 | 0 |

| 1 | 2019-01-07 | 2 | 0 | 0 |

| 2 | 2019-01-07 | 3 | 0 | 0 |

| 3 | 2019-01-07 | 4 | 0 | 0 |

| 4 | 2019-01-07 | 5 | 0 | 0 |

| ... | ... | ... | ... | ... |

| 304388 | 2020-12-14 | 1105 | 0 | 1 |

| 304389 | 2020-12-21 | 831 | 0 | 1 |

| 304390 | 2020-12-21 | 1203 | 0 | 1 |

| 304391 | 2020-12-21 | 2540 | 0 | 1 |

| 304392 | 2020-12-28 | 831 | 0 | 1 |

304393 rows × 4 columns

merged_df_without_removed_outliers = new_df_merged.copy()

Awareness of removing outliers

For some data, the removing is quite agressive, and cause the model error in fitting.

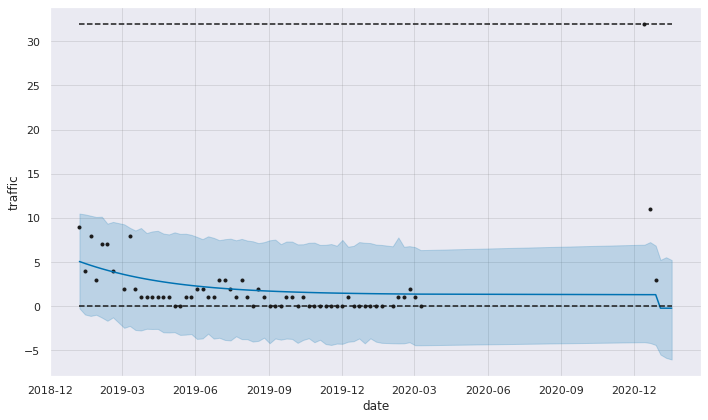

new_df = merged_df_without_removed_outliers.loc[merged_df_without_removed_outliers['product_id'] == 45]

m = fbprophet.Prophet(growth='logistic')

#m.add_regressor('traffic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'traffic': 'y'})

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

fcst1 = m.predict(future)

fig1 = m.plot(fcst1, ylabel='traffic', xlabel='date')

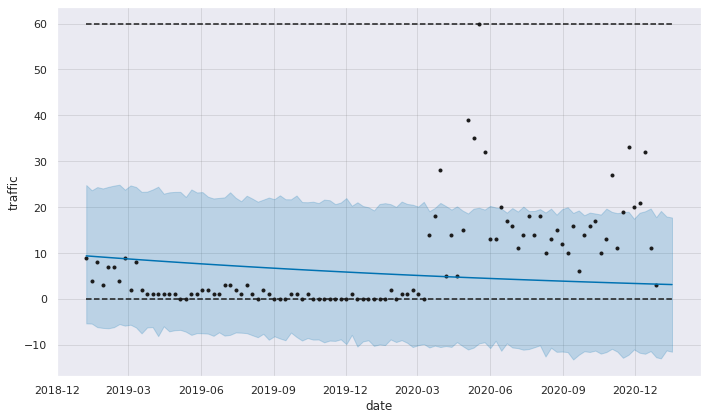

# Removing outliers by calculating 0.95 quantile per product

new_df_merged_filled_zeros = remove_outliers(merged_df_without_removed_outliers, 'traffic')

new_df_merged_filled_zeros.loc[new_df_merged_filled_zeros['product_id'] == 45]

| week_starting_date | product_id | sales | traffic | |

|---|---|---|---|---|

| 40 | 2019-01-07 | 45 | 18 | 9 |

| 2966 | 2019-01-14 | 45 | 22 | 4 |

| 5892 | 2019-01-21 | 45 | 15 | 8 |

| 8818 | 2019-01-28 | 45 | 24 | 3 |

| 11744 | 2019-02-04 | 45 | 13 | 7 |

| ... | ... | ... | ... | ... |

| 175600 | 2020-03-02 | 45 | 9 | 1 |

| 178526 | 2020-03-09 | 45 | 20 | 0 |

| 295566 | 2020-12-14 | 45 | 147 | 32 |

| 298492 | 2020-12-21 | 45 | 56 | 11 |

| 301418 | 2020-12-28 | 45 | 4 | 3 |

63 rows × 4 columns

# Using the same parameters, but with removed outliers

new_df = new_df_merged_filled_zeros.loc[new_df_merged_filled_zeros['product_id'] == 45]

m = fbprophet.Prophet(growth='logistic')

#m.add_regressor('traffic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'traffic': 'y'})

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

fcst1 = m.predict(future)

fig1 = m.plot(fcst1, ylabel='traffic', xlabel='date')

WARNING:fbprophet.models:Optimization terminated abnormally. Falling back to Newton.

---------------------------------------------------------------------------

RuntimeError Traceback (most recent call last)

/usr/local/lib/python3.7/dist-packages/fbprophet/models.py in fit(self, stan_init, stan_data, **kwargs)

244 try:

--> 245 self.stan_fit = self.model.optimizing(**args)

246 except RuntimeError:

/usr/local/lib/python3.7/dist-packages/pystan/model.py in optimizing(self, data, seed, init, sample_file, algorithm, verbose, as_vector, **kwargs)

580

--> 581 ret, sample = fit._call_sampler(stan_args)

582 pars = pystan.misc._par_vector2dict(sample['par'], m_pars, p_dims)

stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.pyx in stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.StanFit4Model._call_sampler()

stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.pyx in stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488._call_sampler()

RuntimeError: Exception: Exception: multiply: B[1] is -nan, but must not be nan! (in 'unknown file name' at line 61)

(in 'unknown file name' at line 121)

During handling of the above exception, another exception occurred:

RuntimeError Traceback (most recent call last)

<ipython-input-46-7b5b9ed0a54e> in <module>()

7 new_df['cap'] = max(new_df.y)

8 new_df['floor'] = 0

----> 9 m.fit(new_df)

10 future = m.make_future_dataframe(3, freq='W')

11 future['cap'] = max(new_df.y)

/usr/local/lib/python3.7/dist-packages/fbprophet/forecaster.py in fit(self, df, **kwargs)

1164 self.params = self.stan_backend.sampling(stan_init, dat, self.mcmc_samples, **kwargs)

1165 else:

-> 1166 self.params = self.stan_backend.fit(stan_init, dat, **kwargs)

1167

1168 # If no changepoints were requested, replace delta with 0s

/usr/local/lib/python3.7/dist-packages/fbprophet/models.py in fit(self, stan_init, stan_data, **kwargs)

250 )

251 args['algorithm'] = 'Newton'

--> 252 self.stan_fit = self.model.optimizing(**args)

253

254 params = dict()

/usr/local/lib/python3.7/dist-packages/pystan/model.py in optimizing(self, data, seed, init, sample_file, algorithm, verbose, as_vector, **kwargs)

579 stan_args = pystan.misc._get_valid_stan_args(stan_args)

580

--> 581 ret, sample = fit._call_sampler(stan_args)

582 pars = pystan.misc._par_vector2dict(sample['par'], m_pars, p_dims)

583 if not as_vector:

stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.pyx in stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.StanFit4Model._call_sampler()

stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488.pyx in stanfit4anon_model_dfdaf2b8ece8a02eb11f050ec701c0ec_4165267599802363488._call_sampler()

RuntimeError: Exception: Exception: multiply: B[1] is -nan, but must not be nan! (in 'unknown file name' at line 61)

(in 'unknown file name' at line 121)

Let’s try to “repair” the model by using different parameter

# Using weekly_seasonality=True parameter, but with removed outliers

new_df = new_df_merged_filled_zeros.loc[new_df_merged_filled_zeros['product_id'] == 45]

m = fbprophet.Prophet(weekly_seasonality=True, growth='logistic')

#m.add_regressor('traffic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'traffic': 'y'})

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

fcst1 = m.predict(future)

fig1 = m.plot(fcst1, ylabel='traffic', xlabel='date')

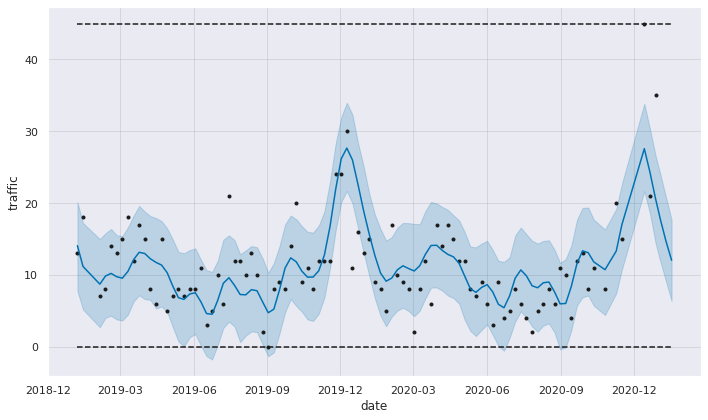

Create first traffic model for chosen product

new_df = new_df_merged_filled_zeros.loc[new_df_merged_filled_zeros['product_id'] == 48]

m = fbprophet.Prophet(yearly_seasonality=True, growth='logistic')

#m.add_regressor('traffic')

new_df = new_df.rename(columns={'week_starting_date': 'ds', 'traffic': 'y'})

new_df['cap'] = max(new_df.y)

new_df['floor'] = 0

m.fit(new_df)

future = m.make_future_dataframe(3, freq='W')

future['cap'] = max(new_df.y)

future['floor'] = 0

fcst1 = m.predict(future)

fig1 = m.plot(fcst1, ylabel='traffic', xlabel='date')

def get_prediction_traffic(df: pd.DataFrame) -> dict:

"""

Create prediction for products traffic

Input:

df: pd.DataFrame

Output:

prediction: dict

"""

prediction = {}

df = df.rename(columns={'week_starting_date': 'ds','traffic': 'y', 'product_id': 'article'})

list_articles = df.article.unique()

for article in list_articles:

if article >= 40:

break

article_df = df.loc[df['article'] == article].copy()

article_df['cap'] = max(article_df.y)

article_df['floor'] = 0

# Check if the cap is equal the floor

if max(article_df.y) != 0:

my_model = fbprophet.Prophet(weekly_seasonality=True,

seasonality_prior_scale=0.1,

growth = 'logistic')

# Filter date from 16 weeks of the last record to last record

# Set cutoff date 3 weeks of the last record

cutoffs = get_date_as_str(df = article_df,

week = 16,

type_return = "type_str")

mask = (article_df['ds'] >=cutoffs)

article_df = article_df.loc[mask]

my_model.fit(article_df)

#df_cv = cross_validation(my_model, initial='548 days', period='180 days', horizon = '21 days')

#df_cv = cross_validation(my_model, initial='695 days', period='7 days', horizon = '21 days')

# Set cutoff date 3 weeks of the last record

cutoffs = get_date_as_str(df = article_df,

week = 3,

type_return = "type_datetime")

df_cv = cross_validation(my_model,

cutoffs=cutoffs,

horizon='21 days',

parallel="processes")

# Round predicted values and replace if is negative

df_cv.yhat = df_cv.yhat.round()

df_cv.yhat = df_cv.yhat.mask(df_cv.yhat.lt(0),0)

del my_model

else:

data = ([['2020-12-14', 0, 0],

['2020-12-21', 0, 0],

['2020-12-28', 0, 0]])

df_cv = pd.DataFrame(data, columns = ['ds', 'y', 'yhat'])

#future_dates = my_model.make_future_dataframe(periods=3, freq='W')

#forecast = my_model.predict(future_dates)

prediction[article] = df_cv

return prediction

predicted = get_prediction_traffic(new_df_merged_filled_zeros)

predicted

{1: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 -0.0 -3.314623e-13 2.645080e-13 0 2020-12-07

1 2020-12-21 0.0 -2.904974e-13 3.490215e-13 0 2020-12-07

2 2020-12-28 0.0 -2.860131e-13 3.413645e-13 0 2020-12-07,

2: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 830.0 794.459264 869.223777 736 2020-12-07

1 2020-12-21 875.0 836.340372 914.276887 147 2020-12-07

2 2020-12-28 903.0 865.593979 941.569269 81 2020-12-07,

3: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 35.0 33.147280 37.067659 14 2020-12-07

1 2020-12-21 53.0 51.047349 55.267420 22 2020-12-07

2 2020-12-28 78.0 76.378858 80.549221 19 2020-12-07,

4: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 0.0 -2.273963e-13 3.414365e-13 0 2020-12-07

1 2020-12-21 -0.0 -3.405071e-13 2.718099e-13 0 2020-12-07

2 2020-12-28 -0.0 -3.044627e-13 3.006419e-13 0 2020-12-07,

5: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 22.0 21.513397 21.513397 26 2020-12-07

1 2020-12-21 22.0 22.271891 22.271891 6 2020-12-07

2 2020-12-28 23.0 22.977895 22.977896 10 2020-12-07,

6: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 55.0 51.653314 57.647132 32 2020-12-07

1 2020-12-21 74.0 70.601456 77.053469 29 2020-12-07

2 2020-12-28 95.0 91.798615 98.174632 35 2020-12-07,

7: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 2.0 0.798409 4.190442 3 2020-12-07

1 2020-12-21 2.0 0.721176 4.372512 1 2020-12-07

2 2020-12-28 2.0 0.608879 4.217207 1 2020-12-07,

8: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 12.0 6.492838 19.032102 0 2020-12-07

1 2020-12-21 14.0 7.711896 20.745267 0 2020-12-07

2 2020-12-28 15.0 8.862105 21.569205 0 2020-12-07,

9: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 9.0 4.960243 12.924439 8 2020-12-07

1 2020-12-21 9.0 5.033804 13.311828 4 2020-12-07

2 2020-12-28 9.0 5.019805 13.090601 1 2020-12-07,

10: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 4.0 1.551638 7.166948 46 2020-12-07

1 2020-12-21 5.0 1.916118 7.364264 19 2020-12-07

2 2020-12-28 5.0 1.990993 7.650544 0 2020-12-07,

11: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 50.0 41.839691 57.891207 17 2020-12-07

1 2020-12-21 55.0 47.522832 64.206855 13 2020-12-07

2 2020-12-28 61.0 52.750043 69.016407 36 2020-12-07,

12: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 1.0 -0.319330 1.360013 0 2020-12-07

1 2020-12-21 1.0 -0.363180 1.385458 0 2020-12-07

2 2020-12-28 0.0 -0.369094 1.314520 0 2020-12-07,

13: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 9.0 7.638626 9.993248 8 2020-12-07

1 2020-12-21 10.0 8.619146 11.153766 3 2020-12-07

2 2020-12-28 11.0 9.657735 12.162501 7 2020-12-07,

14: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 8.0 2.894972 13.330127 2 2020-12-07

1 2020-12-21 8.0 2.997946 14.230813 0 2020-12-07

2 2020-12-28 9.0 2.994879 14.095436 1 2020-12-07,

15: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 96.0 61.003090 129.902303 77 2020-12-07

1 2020-12-21 99.0 66.243308 134.836657 17 2020-12-07

2 2020-12-28 101.0 65.724479 133.909778 29 2020-12-07,

16: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 10.0 8.978201 10.776055 6 2020-12-07

1 2020-12-21 11.0 9.777220 11.706446 10 2020-12-07

2 2020-12-28 11.0 10.227846 12.120446 10 2020-12-07,

17: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 17.0 3.075580 31.353102 7 2020-12-07

1 2020-12-21 17.0 3.515071 32.906864 18 2020-12-07

2 2020-12-28 18.0 3.649959 32.305973 20 2020-12-07,

19: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 22.0 14.911196 29.806150 24 2020-12-07

1 2020-12-21 23.0 15.233583 30.895302 11 2020-12-07

2 2020-12-28 24.0 16.479201 31.870288 8 2020-12-07,

20: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 5.0 1.601734 7.943625 11 2020-12-07

1 2020-12-21 3.0 0.338973 6.611043 4 2020-12-07

2 2020-12-28 3.0 -0.570450 5.801675 2 2020-12-07,

21: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 8.0 5.568788 10.488612 14 2020-12-07

1 2020-12-21 8.0 5.872692 11.168610 2 2020-12-07

2 2020-12-28 9.0 6.136933 11.370472 8 2020-12-07,

22: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 1.0 -1.117006 2.668953 5 2020-12-07

1 2020-12-21 1.0 -1.315457 2.665397 0 2020-12-07

2 2020-12-28 1.0 -1.276621 2.635443 0 2020-12-07,

23: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 -0.0 -2.393039 1.829387 2 2020-12-07

1 2020-12-21 -0.0 -2.541668 2.003540 0 2020-12-07

2 2020-12-28 -0.0 -2.714260 1.777411 0 2020-12-07,

24: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 1.0 -0.372922 2.644378 3 2020-12-07

1 2020-12-21 1.0 -0.459426 2.788531 0 2020-12-07

2 2020-12-28 1.0 -0.574293 2.635407 3 2020-12-07,

25: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 14.0 10.994052 16.083686 9 2020-12-07

1 2020-12-21 14.0 11.444107 16.922816 5 2020-12-07

2 2020-12-28 15.0 11.811661 17.225838 4 2020-12-07,

26: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 0.0 -0.217918 0.444932 0 2020-12-07

1 2020-12-21 0.0 -0.215928 0.473042 2 2020-12-07

2 2020-12-28 0.0 -0.219867 0.451856 3 2020-12-07,

27: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 -0.0 -1.417694e-13 5.899911e-14 7 2020-12-07

1 2020-12-21 0.0 -8.416815e-14 1.170978e-13 0 2020-12-07

2 2020-12-28 0.0 -7.557096e-14 1.312115e-13 0 2020-12-07,

28: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 10.0 9.515788 10.598433 13 2020-12-07

1 2020-12-21 11.0 10.313969 11.392127 2 2020-12-07

2 2020-12-28 11.0 10.896219 11.947059 1 2020-12-07,

29: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 0.0 -7.185052 -1.912559 63 2020-12-07

1 2020-12-21 0.0 -7.486661 -2.053196 18 2020-12-07

2 2020-12-28 0.0 -7.507756 -1.908504 0 2020-12-07,

30: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 7.0 3.507970 9.785503 6 2020-12-07

1 2020-12-21 7.0 3.299814 10.057230 3 2020-12-07

2 2020-12-28 6.0 3.028469 9.706291 6 2020-12-07,

32: ds y yhat

0 2020-12-14 0 0

1 2020-12-21 0 0

2 2020-12-28 0 0,

33: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 3.0 0.537796 5.481520 6 2020-12-07

1 2020-12-21 3.0 0.424975 5.729947 0 2020-12-07

2 2020-12-28 3.0 0.394756 5.599013 2 2020-12-07,

34: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 1.0 -0.451206 2.926333 3 2020-12-07

1 2020-12-21 1.0 -0.409944 2.866366 0 2020-12-07

2 2020-12-28 1.0 -0.302364 2.931885 3 2020-12-07,

37: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 2.0 -0.242928 3.351227 11 2020-12-07

1 2020-12-21 2.0 -0.092053 3.760037 0 2020-12-07

2 2020-12-28 2.0 -0.046679 3.762158 1 2020-12-07,

38: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 0.0 -0.979372 1.605552 0 2020-12-07

1 2020-12-21 0.0 -1.081830 1.609755 0 2020-12-07

2 2020-12-28 0.0 -1.121827 1.469671 0 2020-12-07,

39: ds yhat yhat_lower yhat_upper y cutoff

0 2020-12-14 57.0 49.005293 64.512700 23 2020-12-07

1 2020-12-21 63.0 55.126692 71.819543 8 2020-12-07

2 2020-12-28 67.0 58.849911 75.346128 10 2020-12-07}

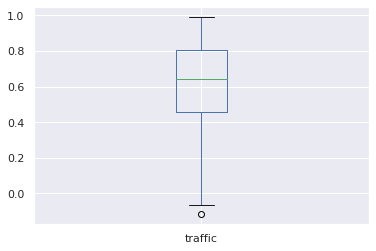

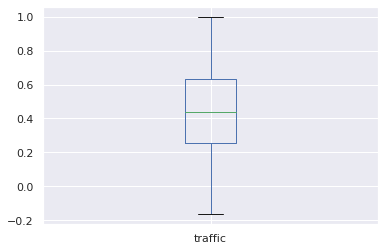

Check correlation betweeen sales and traffic

original_df_corr = (merged_df_without_removed_outliers

.groupby('product_id')

[['sales','traffic']].corr().iloc[0::2,-1])

original_df_corr.plot.box()

<matplotlib.axes._subplots.AxesSubplot at 0x7f89c665ce90>

shifted_df = merged_df_without_removed_outliers.copy()

shifted_df['sales'] = shifted_df.groupby('product_id')['sales'].shift().fillna(0)

corr_df = shifted_df.groupby('product_id')[['sales','traffic']].corr().iloc[0::2,-1]

corr_df.plot.box()

<matplotlib.axes._subplots.AxesSubplot at 0x7f89c65a8490>

Based on the results, there is a lower correlation (median <0.5) if the sales column values are shifted down (than without shifted values). That means we could not have a higher chance that viewers on the website can buy a product in the next week.

Conclusions

Recommendations for estimating future sales:

- If the article is not available at a warehouse and the local branches do not have this article, the forecast should be set to zero. For us it is obvious, but for the model, it is unknown that our supplier does not have such a product.

- If the product sales for six weeks before are equal to zero, the forecast should be set to zero. This range has been chosen arbitrarily.

- When a new product is in our store, we can make some estimations by using category and compare to the same level price products from the same category.

- Campaign marketing actions should be considered when the forecast is evaluated. It is known that the advertisements give more chance for the client’s choice of buying product.

- Based on the observations for some products, the modeling should be done in two ways: by using yearly_seasonality for the whole data from two years and weekly_seasonality for the short data range (it could be last X months)

import sys

print(sys.version)

3.7.10 (default, May 3 2021, 02:48:31)

[GCC 7.5.0]

pip freeze --local > /content/gdrive/My\ Drive/Prediction_task/colab_installed.txt